Faster payment systems, also known as real-time or instant payments, are rapidly becoming a global standard for both retail and business transactions. These systems enable fund availability in real time or near real time on a 24/7/365 basis, with estimates around 100 jurisdictions have introduced or are developing them.

The pace of evolution in instant payments has been remarkable, especially significant in emerging markets, where they have acted as a catalyst for economic activity. Central Banks, regulators and national payment operators worldwide continue to invest in fast payment infrastructure as part of wider digital transformation efforts, while institutions such as the World Bank and the Bank for International Settlements (BIS) continue to document design choices, adoption patterns, and policy considerations.

Key insights from recent reports include:

“Third-party initiation services centralized through the Fast Payments System benefit from existing network effects, which can lead to synergies that boost adoption of both fast payments and open banking services.” (1)

“Fast payments have achieved mass adoption in some jurisdictions but not in others—with adoption likely depending on the design characteristics of different Fast Payments System.” (2)

“Retail payment trends such as digital lending and deferred payments present an opportunity to payment schemes, financial institutions, and overlay services to monetize and increase their customer base by offering services above and beyond the reach of traditional payment channels.” (3)

“Interlinking arrangements among fast payment systems (FPS) are one of the most promising solutions for enhancing cross-border payments, offering the prospect of significantly faster, cheaper, more accessible and transparent cross-border payments.” (4)

Many countries have already launched diverse use cases on instant payment platforms. These are being adopted by banks, financial institutions, and fintech’s to provide cost-effective alternatives with full flexibility over payment orchestration and service delivery. Once a domestic system stabilizes, cross-border payments become a natural extension, leveraging existing rails, customer familiarity, and proven operational models.

Consumer demand is accelerating the shift toward faster, more transparent, and more convenient cross-border payments, as transaction volumes and values continue to rise. The market is projected to grow from USD 397.37 billion in 2026 to USD 727.74 billion by 20345, reflecting rising expectations for seamless international payment experiences. At the same time, the increasing adoption of digital wallets and mobile-first payment journeys is driving growth in both consumer-to-business (C2B) and consumer-to-consumer (C2C) transactions. In practice, the most visible cross-border use cases today include C2C remittances and merchant payments enabled through QR codes or e-commerce channels. Their significance is reflected in projected transaction values, with C2B expected to reach approximately USD 5.15 trillion in 2026 and C2C projected at USD 2.25 trillion. (5)

Project Nexus: A Multilateral Model for Interoperability

A notable global initiative in this space is Project Nexus. Designed as a multilateral framework for connecting domestic instant payment systems across countries, enabling users to send cross-border payments using simple identifiers such as mobile numbers, virtual address or merchant IDs. Developed by the BIS Innovation Hub Singapore Centre in 2021, Nexus has evolved from a proof-of-concept into a live implementation. (6)

Its primary value proposition lies in standardization. Instead of building multiple bilateral connections, each payment system connects once to the Nexus network, instantly gaining access to all participating countries. To operationalize the framework, central banks from India, Singapore, Malaysia, the Philippines, Thailand, and Indonesia established Nexus Global Payments (NGP), an independent not-for-profit entity responsible for governance and rule-setting. (6)

Beyond Nexus, several regional initiatives particularly across Asia-Pacific, Southeast Asia, and Africa, are piloting bilateral cross-border instant payment integrations.

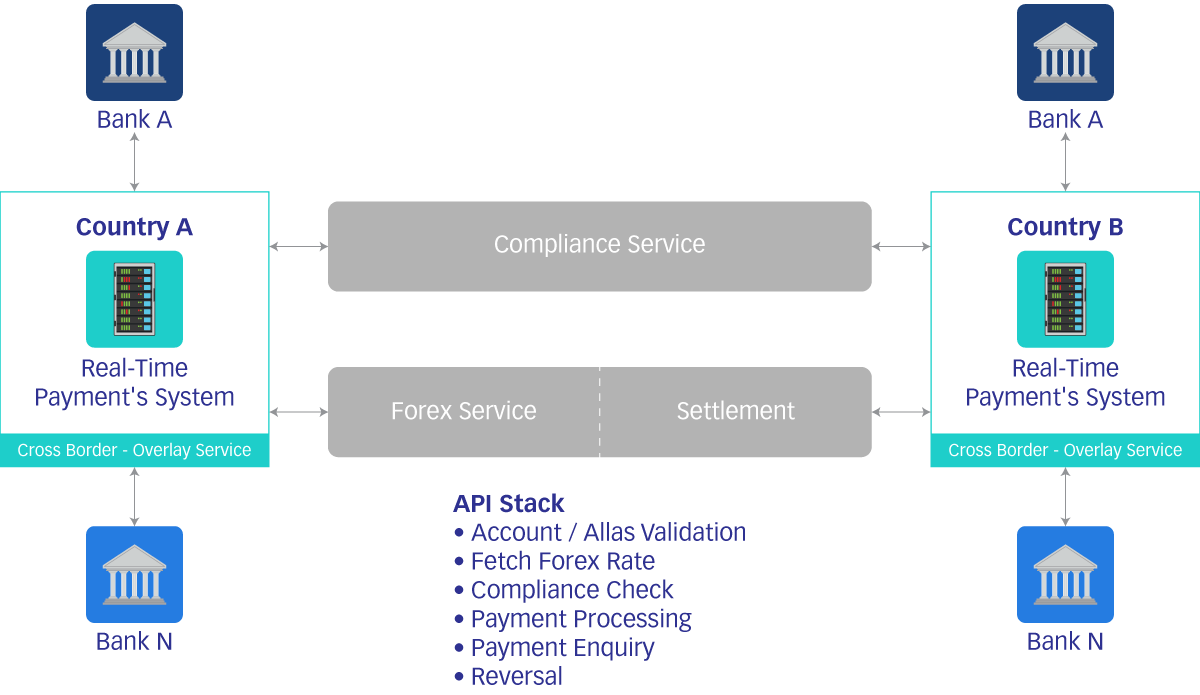

Cross-Border Instant Payment Architecture

Beyond last-mile connectivity managed by domestic instant payment systems, cross-border payments rely on three critical components: funding and settlement, foreign exchange (FX), and compliance screening. An effective system should use a service-based architecture that allows seamless integration of these components.

1. Funding & Settlement

In domestic interbank payments, settlement is typically managed by central banks through RTGS systems. However, cross-border payments introduce additional complexity because liquidity, jurisdictional boundaries, and settlement timing must all be managed across multiple participants and currencies. Several models exist:

- Pre-Funding: Participants hold funds in a nostro account in the destination country. This reduces credit risk but ties up liquidity.

- Netting: Payment obligations are offset over time, with only net balances settled. This can improve efficiency, but it requires robust legal, operational, and risk arrangements.

- Atomic Settlement: A modern approach where both sides of a transaction settle simultaneously and irrevocably. This eliminates settlement risk but introduces technical complexity and may impact processing time.

2. Foreign Exchange (FX)

Foreign exchange is often the largest hidden cost in cross-border payments and significantly affects affordability. Regulators may consider controlling FX markups to ensure competitiveness and transparency for end users.

3. Compliance & Sanction Screening

Compliance remains a non-negotiable component of cross-border payments, ensuring both legality and security. However, processes must be streamlined to avoid duplication. Key requirements typically include:

- KYC (Know Your Customer): Managed by regulated entities in both sending and receiving countries.

- Customer due diligence (CDD) and enhanced due diligence (EDD): Ongoing monitoring, particularly for high-risk transactions, including screening against global sanctions lists such as OFAC, UN, and EU.

- Sanction Screening and AML controls: Required to ensure payments meet legal and regulatory obligations.

Key Innovation Drivers

Several technology enablers are helping shape the next phase of cross-border instant payments:

- API-based Platforms: Allow seamless embedding of payments, FX, and compliance services into financial applications.

- RegTech Solutions: more advanced compliance technologies and shared utilities streamline compliance processes, reducing cost and delays.

- Blockchain and DLT-based models: Enables atomic settlement and transparent audit trails.

Conclusion

Effective cross-border instant payments depend on selecting the right funding and settlement mechanisms to balance cost and speed, ensuring transparent and competitive FX rates, and integrating robust yet efficient compliance processes.

The evolution of the cross-border payments landscape continues to focus on making these elements faster, more transparent and more interoperable. While initiatives such as Project Nexus may take time to achieve widespread adoption, regulators and policymakers can make meaningful progress optimizing high-volume payment corridors, strengthening bilateral arrangements, and designing architectures that are modular enough to support broader interoperability over time.

References

- World Bank. Open Banking and the Future of Fast Payment Systems (2023)

https://fastpayments.worldbank.org/sites/default/files/2023-09/Open%20Banking%20and%20FPS_Final_August%2028.pdf - Bank for International Settlements. Fast Payments: Design and Adoption (2024)

https://www.bis.org/cpmi/publ/d216.pdf - World Bank. The Future of Fast Payments (2023)

https://fastpayments.worldbank.org/sites/default/files/2023-10/Future%20of%20Fast%20Payments_Final.pdf - BIS Committee on Payments and Market Infrastructures (CPMI). Linking Fast Payment Systems Across Borders (2023)

https://www.bis.org/cpmi/publ/d215.pdf - Fortune Business Insights. (2026). Cross border payment market size, share & growth [2026–2034]. Fortune Business Insights.

https://www.fortunebusinessinsights.com/cross-border-payments-market-110223 - World Bank. (n.d.). Project FASTT (Frictionless Affordable Timely Transactions) – retail fast payments. World Bank Fast Payments Tracker.

https://fastpayments.worldbank.org