We are witnessing a profound transformation in the architecture of global finance. What began as independent initiatives in different markets has evolved into a broader global movement. Open banking, instant payment networks, and digital currency initiatives are no longer isolated developments; together, they are reshaping financial ecosystems to become faster, more transparent, and more inclusive. From Lagos to London and Mumbai to Mexico City, the contours of this shift reality are visible today.

Open Banking: From Regional Experiment to Global Momentum

A decade ago, open banking was largely associated with a few European markets. Today, it has become a global standard embraced by governments, regulators, and financial institutions worldwide. Over seventy-eight jurisdictions have either implemented open banking frameworks or are advancing regulatory infrastructures to support them[1].

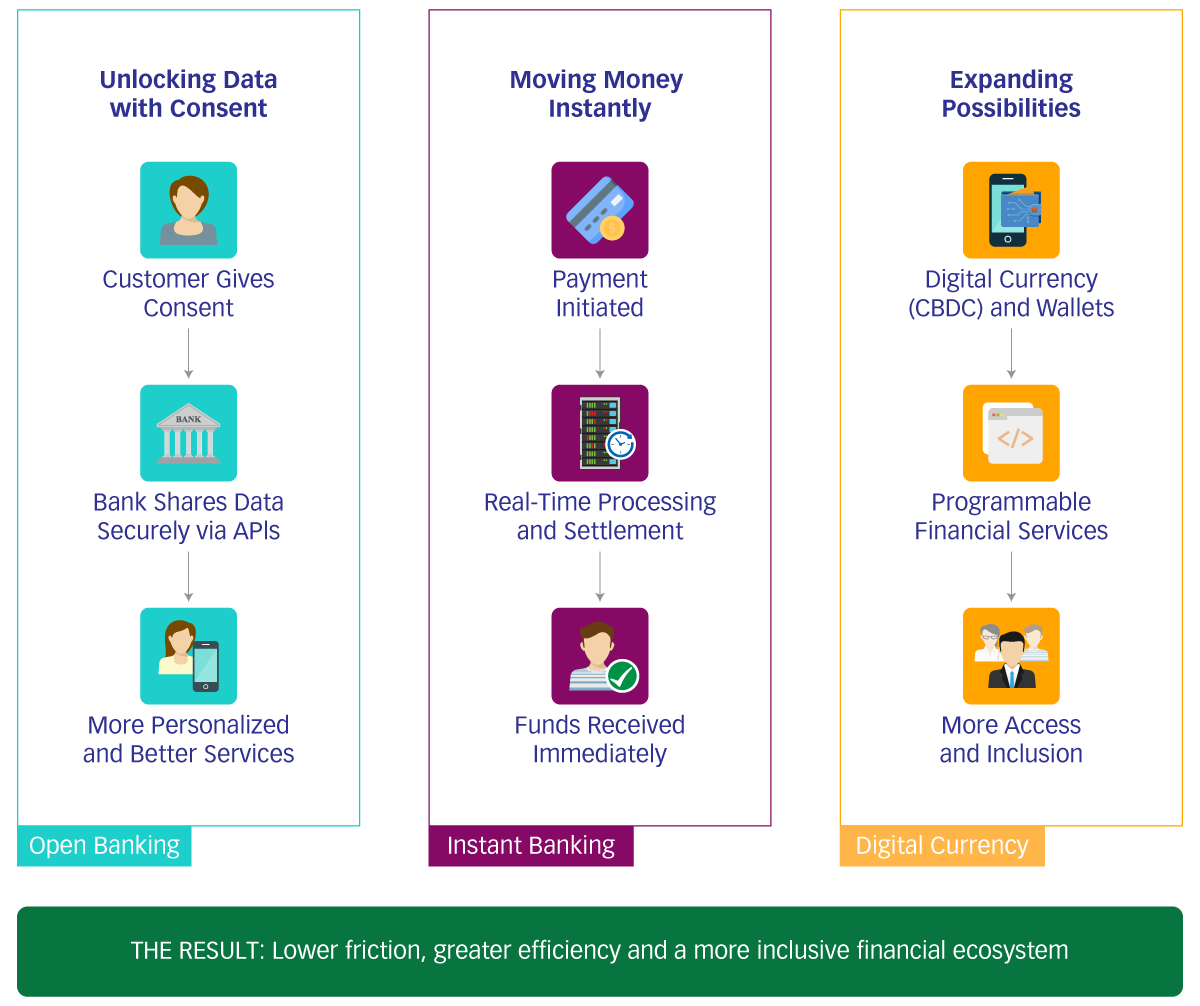

Open banking rests on a simple but transformative premise: individuals and businesses should have sovereign, consent based control of their financial data through standardized, secure APIs. This shifts the power away from closed systems and toward more competitive, customer-driven financial services.

Empirical evidence underscores the impact of open banking. In the United Kingdom alone, over 15 million active users are engaged with open banking services, while successful global API transaction volumes have surpassed 120 billion annually[1]. In emerging markets, open APIs are stimulating innovation and inclusion by enabling neobanks and embedded finance platforms to reach previously underserved populations.

Open banking does not replace traditional financial institutions. Instead, it pushes the market toward better customer experiences, more relevant services, and greater operational efficiency. When financial data can be securely shared with permission, it creates stronger foundations for personalized services, improved financial visibility, and more seamless digital journeys.

Instant Payments: Redefining the Speed of Transactions

If open banking unlocks the movement of data, instant payments networks energize the movement of money. These systems have become core financial infrastructure, facilitating real-time settlement and fundamentally altering expectations about how transactions should operate.

The significance of these systems extends well beyond convenience. They help businesses improve liquidity management, allow workers and merchants to access funds faster, and strengthen the usability of digital financial services. In many markets, they also support lower-cost alternatives to cash and traditional payment rails.

Brazil offers one of the strongest examples. By late 2025, the Banco Central do Brazil reported that Pix had reached nearly 170 million users, underlining how quickly an instant payment scheme can become embedded in everyday economic activity when it is simple, accessible, and widely accepted[2].

Comparable systems across other markets reinforce the same direction:

- Europe’s Single Euro Payments Area (SEPA) Instant Credit Transfer provides real-time settlement across many EU member states.

- The United Kingdom’s Faster Payments Service has driven widespread use of real time transfers.

- In Asia, Singapore’s PayNow and Thailand’s PromptPay have become core elements of national payment infrastructures.

These platforms are increasingly interconnected, laying the groundwork for regional and, eventually, global payment flows.

Central Bank Digital Currencies: From Exploration to Early Implementation

Central Bank Digital Currencies (CBDCs) represent a critical evolution in how public authority interfaces with financial exchange. What was once a theoretical discussion is now an active area of policy and infrastructure development. More than 130 countries and currency unions are actively researching, piloting, or deploying CBDCs as part of broader modernization strategies[3].

Several countries, including the Bahamas, Jamaica, Nigeria, and members of the Eastern Caribbean Currency Union, have operational retail CBDCs. These national systems are expanding access, reducing transaction costs, and enabling programmable financial capabilities that were not possible under traditional fiat frameworks.

In specific contexts, CBDCs may help expand access, improve payment resilience, support public-sector disbursements, and enable new forms of programmable financial functionality. Their long-term relevance will depend not only on design, but also on how well they integrate with broader payment and financial infrastructure.

When CBDCs initiatives are viewed alongside open banking and instant payments, the bigger picture becomes clearer: financial systems are moving toward greater interoperability, faster execution, and more digitally native service delivery.

The Gradual Retreat of Cash

The notion that cash is obsolete is an overstatement. A more accurate characterization is that in many markets, cash is gradually becoming less central to everyday use as digital alternatives become more accessible, convenient and efficient.

Real-time payment systems and digital transaction platforms have reduced dependence on physical currency in mature and emerging markets alike. Where digital channels are trusted, easy to use, and widely accepted, behavior tends to shift naturally.

Cash remains indispensable in specific contexts such as during power disruptions, for populations with limited digital literacy, and in crisis environments. However, the broader trend toward digital payments are taking a larger share of routine financial activity, and the COVID 19 pandemic accelerated this progression by familiarizing billions with contactless payments, QR codes, and mobile financial interfaces, reinforcing that physical currency is often slower and riskier for routine transactions.

Frictionless Finance for Everyone

Three enduring trends now define the evolution of finance:

- Open Banking: Individuals and businesses exercise control over their financial data, fostering innovation and competition.

- Instant Payments: Funds move in real-time, aligning financial services with the expectations of a connected economy.

- Digital Currencies and Wallets: Programmable, inclusive, and interoperable financial instruments provide new avenues for economic participation.

Together, these forces are reshaping the global financial landscape, enhancing efficiency, expanding access, and redefining how value is created, transferred, and experienced.

Conclusion: Beyond Cash and Borders

The future of finance will not be defined by a contest between cash and digital alternatives. Instead, it will be shaped by systems that move value seamlessly, inclusively, and at scale. Digital exchange will become the default mode for everyday transactions, enabling instantaneous settlements, universal access, and financial tools that adapt to individual and institutional needs with precision.

Barriers that once constrained global financial participation (geographic, economic, technological) are dissolving. In their place there is a landscape characterized by speed, transparency, and fairness. The era of frictionless finance is not a distant aspiration; it is the emerging reality of financial systems around the world.

References:

- CoinLaw. (2025, July 5). Open Banking Adoption Statistics 2026: Adoption, Innovation & Growth. https://coinlaw.io/open-banking-adoption-statistics

- Bank for International Settlements. (2024, November 21). Retail fast payment systems as a catalyst for digital finance. https://www.bis.org/publ/work1228.pdf

- Atlantic Council. (2026). Central Bank Digital Currency Tracker. https://www.atlanticcouncil.org/cbdctracker