January 10, 2023

Why CBDC is Also a Commercial Bank Digital Currency

Hussein Jundi

Share Article

Estimates show that almost 90% of central banks around the world have embarked on their journey towards introducing a central bank digital currency (CBDC). Current results and expectations are promising in terms of enhancing monetary policies, financial inclusion, interoperability and more, all of which are nationwide achievements.

However, most research on CBDC is focused on the implications that the technology imposes on central banks. While the first two words of CBDC relate to central banks, they are not the sole stakeholders of the technology. But where do commercial banks and other financial institutions fit into this disruptive transformation, what will their role look like, and why is there little input from those entities in central bank publications and research developments?

The responsibilities of central banks widely differ from one country to another. In general, one of its most important duties is the control and manipulation of the money supply in issuing the currency. Therefore, it goes without saying that as the issuer of a country’s currency, the central bank is the main stakeholder. Nonetheless, after issuing the money, the financial ecosystem relies heavily on commercial banks and financial institutions to distribute and maintain the money for the general population.

According to most CBDC study cases and for the purposes of this article, we will assume that the same scenario applies in which the central bank opts for the two-tier model where commercial banks are the go-to entities for financial matters. After all, CBDC is designed to digitally represent and mimic cash in every way possible.

As a prerequisite to implementing a CBDC with countrywide access, the central bank is responsible for properly assessing the need for CBDC, taking into consideration all the different factors. Some of these considerations relate to infrastructure capabilities, existing payment systems, acceptance of digital payments and more. Accordingly, the central bank should decide on a suitable roll-out plan and technology to achieve its targets. Achieving these targets and delegating to all the players in the ecosystem requires a lot of effort, therefore, some responsibilities should be handled by other vital organizations for proper facilitation.

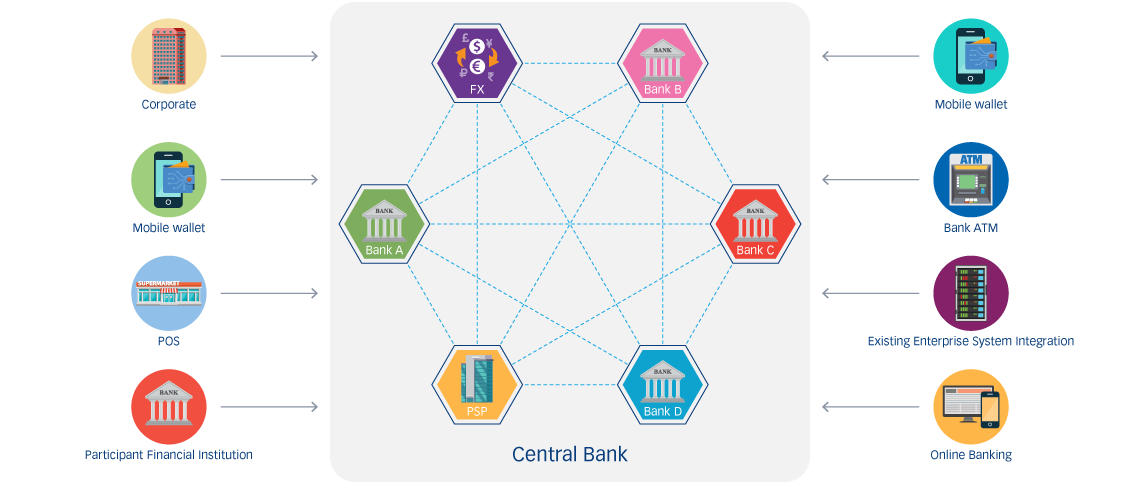

Commercial banks are equipped with the capability and experience to accommodate customers’ needs, as people are generally used to dealing with banks for financial matters. In the two-tier model where the central bank mints and issues CBDC units, commercial banks will have to exchange a form of currency with the central bank in exchange for CBDC, a process we call pledging. Once the CBDC units are with the commercial bank, the role of distributing these units for general use relies on these commercial banks. In wholesale CBDC, commercial banks are of course an integral part of the ecosystem. Even in the retail model, commercial banks are as integral since they have a large responsibility of being the customer-facing entities for CBDC as custodians for the wallets and its distribution among the public.

With the enrollment of CBDC, we must face the fact that it has both its advantages and disadvantages. The advantages of having CBDC for commercial banks must be communicated and explained in a detailed manner. Some of these advantages for commercial banks include cost reduction from the high transaction fees and cost of handling cash. CBDC will also increase the customer base as more unbanked and underbanked individuals will be striving to gain more access to financial services and there is a large market need for such innovations. This goes hand in hand with the rise of fintech solutions and cryptocurrencies that are already tempting people to steer away from traditional banking services. In addition, it has many indirect advantages as CBDC promises resilience and a high level of security, therefore decreasing the number of potential financial crimes and encouraging customers to remain loyal to the bank.

The need for commercial banks goes even beyond these obvious gains. As trusted entities by governmental and private institutions, it is most likely that commercial banks will be the validating nodes for the transactions done on the CBDC network. If the central bank opts for the distributed ledger technology (DLT) version, the role of commercial banks will be vital in giving their consensus and having a copy of the ledger for safekeeping. That being said, preparations on the commercial bank side are crucial; they should start working on understanding the needs that will be requested from them and prepare accordingly. This is an intricate task that requires the same level of assessment that a central bank will have in terms of considering integration with existing payments infrastructure, both in its front and back ends.

To conclude, while the name implies that it is a central bank digital currency, it is also a commercial bank digital currency. Central banks should include commercial banks in the early stages of research and development to properly assess how they can benefit each other by learning what their specific needs are. The input that can be generated by this collaboration will clear the cloudiness on the road ahead and guarantee alignment between the vital stakeholders. It is important to engage and communicate with all relevant stakeholders to promote a full understanding of how CBDC will change the banking ecosystem, and to align for what is to come.